Coronavirus 2019/COVID-19 Resource Page

Page last updated: December 22, 2020.

For information on how our state is responding to the Coronavirus outbreak, and the latest actions from Governor Lamont and state agencies, please visit: ct.gov/coronavirus.

For the latest updates from the Centers for Disease Control and Prevention on the virus, visit: cdc.gov/coronavirus.

Resources for Families, Workers, Small Businesses and More

In March, Congress passed three measures designed to respond to state and local public health needs and financial needs of families, community organizations, and small businesses. This resource page aims to provide easy access to the latest information on how to access programs and agencies. If you have additional questions or need assistance after reviewing this page, you can contact my office at (860) 886-0139.

Recent Omnibus COVID-19 Relief Bill Information

COVID-19 Testing in Eastern Connecticut

Unemployment Insurance

Direct Payments to Families and Individuals

Resources for Small Businesses

Paid Leave for Working Americans

Resources for Student Loan Borrowers

Food Assistance and Food Banks

Important Information for Veterans

Homeowner & Renters Insurance

Support for Eastern Connecticut Farmers

Legislative Action & Press Releases

Recent Omnibus COVID-19 Relief Bill Information

On December 21st, 2o20, the House passed the 2021 Consolidated Appropriations Act (H.R. 133), a bipartisan omnibus agreement that includes long-awaited COVID-19 relief provisions, and that would avoid a looming government shutdown. The agreement includes relief provisions that the House has fought for months to secure through bills like the HEROES Act, including a new round of forgivable PPP loans, strong support for restaurants and other small businesses, enhanced unemployment insurance, new rental assistance, and much more. H.R. 133 includes resources that are urgently needed to address the national response to COVID-19 and to the economic fallout it has caused, such as:

- Acceleration of vaccine distribution and crushing the coronavirus — The bipartisan relief package provides billions in urgently needed funds to accelerate the free and equitable distribution of safe vaccines to as many Americans as possible as soon as possible, to implement a strong national testing and tracing strategy, and to support our heroic health care workers and providers.

- Strong support for restaurants and other small business — The relief package secures critical funding and policy changes to help small businesses and nonprofits recover from the pandemic. H.R. 133 includes over $284 billion for first and second forgivable PPP loans, expanded PPP eligibility for nonprofits and local newspapers, TV and radio broadcasters, key modifications to PPP to serve the smallest businesses and struggling non-profits and better assist independent restaurants, and includes $15 billion in dedicated funding for live venues, independent movie theaters, and cultural institutions. The agreement also includes $20 billion for targeted EIDL Grants which are critical to many smaller businesses on Main Street.

- Rental assistance — The new relief package secures $25 billion in critically needed rental assistance for families struggling to stay in their homes and an extension of the eviction moratorium.

- Direct payment checks — The bill includes a new round of direct payments worth up to $600 per adult and child, also ensuring that mixed-status families receive payments.

- Strengthened Earned Income Tax Credit & Child Tax Credit — The agreement helps ensure that families who faced unemployment or reduced wages during the pandemic are able to receive a strong tax credit based on their 2019 income, preserving these vital income supports for vulnerable families.

- Supports paid sick leave — The agreement provides a tax credit to support employers offering paid sick leave, based on the Families First Act framework.

- Employee Retention Tax Credit — The agreement extends and improves the Employee Retention Tax Credit to help keep workers in jobs during coronavirus closures or reduced revenue.

- Enhanced Unemployment Insurance benefits — H.R. 133 averts the sudden expiration of Unemployment Insurance benefits for millions of Americans, and adds a $300 per week UI enhancement for Americans out of work.

- Nutrition assistance for hungry families — The agreement provides $13 billion in increased SNAP and child nutrition benefits to help relieve the historic hunger crisis that has left up to 17 million children food insecure.

- Education and child care — The bill provides $82 billion in funding to state, school districts and colleges, including support for HVAC repair and replacement to mitigate virus transmission and reopen classrooms, and $10 billion for child care assistance to help get parents back to work and keep child care providers open.

Please check back later for more information and resources on how to apply for this assistance.

COVID-19 Testing in Eastern Connecticut

To look up your nearest COVID-19 testing location by zip-code, and for information on how to register for a test, click here.

- Community Health Center Inc. offers free, walk-up and drive-up COVID-19 testing across eastern Connecticut. While no symptoms or appointment is necessary, pre-registration is encouraged. For a full schedule or to register for testing, call 475-241-0740 or click here.

- UCFS Healthcare offers daily, free, drive-up COVID-19 at the Griswold Health Center in Griswold and the Edward & Mary Lord Family Health Center in Norwich, as well as various pop-up locations across eastern Connecticut. No appointment is necessary. For a full schedule and more information, click here.

- Hartford Health Care has recently expanded their COVID-19 testing capabilities. Backus Hospital has moved their drive-up testing site, open 7 days a week from 8 AM - 4 PM, to Dodd Stadium in Norwich. For more information, and for additional testing sites throughout the state, click here.

- Generations Health Care is offering drive-up COVID-19 testing at their Danielson, Putnam, and Willimantic sites. For more information on how to register, click here.

Unemployment Insurance

Congress approved legislation to improve unemployment benefits, including providing an additional $600 per week for four months, providing an additional 13 weeks of federally funded benefits, and expanding eligibility to include more workers. These benefits are available immediately, subject to implementation from the Connecticut Department of Labor (CT DOL).

Important Information for you to know:

- The Unemployment Insurance program is administered by CT DOL. While there is a delay in the Department's ability to process claims, eligible individuals are encouraged to apply here: http://www.ctdol.state.ct.us/UI-online/Index.htm

- Due to the widespread economic impact of this pandemic, Connecticut's unemployment system has been inundated with new applications. Typically CT DOL receives 3,000 new claims a week; in the recent it has received more than 200,000 claims – more than one year's worth of claims in just over two weeks. Currently there is a five-week backlog for processing claims, however, CTDOL is working to reduce that wait time.

- If you have trouble accessing the system, please be patient and keep trying. Regardless of when your application is processed, you will receive retroactive compensation from the date you filed. For the latest updates on Connecticut's unemployment program, click here for a regularly updated FAQ from CT DOL.

- Those who are self-employed, gig workers, independent contractors, and others not traditionally eligible for unemployment are now eligible for the Pandemic Unemployment Assistance program. Please note that the system for filing and processing claims under this new program is not yet in place in Connecticut, and CT DOL recommends that self-employed and independent contractors wait until the PUA system is up and available to take claims before first applying for regular benefits.

- CTDOL has launched the new portal for self-employed individuals seeking to file for Pandemic Unemployment Assistance (PUA) – the additional $600 of unemployment assistance Congress voted to authorize with the bipartisan CARES Act. To reach the tool, visit www.filectui.com and click on the red button labeled "PUA designation". Once you've reached the FAQ page, select "INSTRUCTIONS, and "FILE PUA" in the grey "PUA Quick Links" box. The portal accepts applications from self-employed individuals, including independent contractors and "gig" workers who have already applied through the state unemployment system, and have received notice from CTDOL.

- The criteria for claiming unemployment compensation has been expanded to capture more workers impacted by COVID-19. For example, if you were planning to start a new job but are no longer able to due to the pandemic, you are eligible for benefits. You will also be covered if you were immediately laid off from a new job and did not have a sufficient work history to qualify for benefits under normal circumstances.

- As a result of the CARES Act, all weekly unemployment benefit payments will be increased by $600. This increased benefit is scheduled to begin April 24, and claimants should begin to see this increase the following week.

Resources

- CT DOL FAQ on Unemployment Assistance

- Committee on Ways & Means fact sheet & FAQ on unemployment compensation

Direct Payments to Individuals and Families

Many individuals and families in eastern Connecticut facing unexpected costs and economic hardship due to the pandemic will receive direct payments from the government (referred to as rebates) to help minimize financial strain during the public health crisis.

Everyone is eligible for rebate payments as long as they have a Social Security Number and their income falls under the threshold outlined below. This includes Social Security beneficiaries (retirement, disability, survivor) and Supplemental Security Income (SSI) recipients. For individuals making $75,000 or less ($150,000 for joint filers), the rebate will be $1,200 ($2,400 for joint filers). The rebate will include an additional $500 for each qualifying minor in the household. For individuals and joint filers making more than the thresholds listed above, the rebate payment will be reduced by $5 for every additional $100 of income made (rebates will completely phase out for incomes over $99,000 for an individual and $198,000 for joint filers).

The IRS has onboarded an additional 3,500 telephone representatives to help answer some of the most common questions regarding Economic Impact Payments. If you are entitled to a stimulus payment but have not received one, you can now call800-919-9835 to inquire.

Important information for you to know:

- These payments are federal rebates, and are not taxable income.

- Rebates will be delivered by the IRS to most Americans who file individual federal income tax returns. When available, electronic direct deposit will be used in place of mailing a physical check.

- If you filed a 2019 or 2018 tax return, your rebate will likely be disbursed automatically. Social Security beneficiaries and SSI recipients who did not file a tax return may need to take additional action, such as filing an abbreviated tax return, to receive a rebate.

- No extra filing for Social Security and SSI beneficiaries: According to a recent announcement by the Treasury Department Social Security beneficiaries and SSI recipients who did not file a tax return will not need to take additional action, such as filing an abbreviated tax return, to receive a rebate. However, because people who receive SSI benefits aren't typically required to file taxes, an extra step is needed in order for SSI recipients to claim the $500 for children under 17. If you or someone you know receives SSI and have children who qualify, make sure to complete this extra step by visiting IRS.gov and clicking on "Non-Filers: Enter Payment Info Here" to get started.

- Current timeline: The IRS is expected to make about 60 million payments to Americans through direct deposit in mid-April (likely, the week of April 13th). The IRS has direct deposit information for these individuals from their 2018 or 2019 tax returns. This will include SSA beneficiaries who filed federal tax returns that included direct deposit information. About 10 days after after the first round of payments are made in mid-April, the IRS plans to make a second run of payments. These payments will be made to SS beneficiaries who did not file tax returns in 2018 or 2019 and receive their Social Security benefits via direct deposit. (The estimates are that nearly 99 percent of SS beneficiaries who do not file a return receive their SS benefits through direct deposit.)

-

SI recipients will receive their automatic payments in early May, and the VA payment schedule for beneficiaries who receive Compensation and Pension (C&P) benefit payments is still being determined.

- Like tax credits, these payments do not count as income or resources for means-tested programs. So receiving a rebate will not interfere with someone's eligibility for SSI, SNAP, Medicaid, ACA premium credits, TANF, housing assistance, or other income-related federal programs.

- These rebates do not affect receipt of state or federal unemployment compensation.

- Dependents: You are currently ineligible to receive a payment if someone else claims you as a dependent (i.e. a college student claimed as a dependent by their parents)

- You are ineligible to receive a payment if someone else claims you as a dependent (i.e. a college student claimed as a dependent by their parents)

- Rebates do not need to be repaid. If an individual experienced an income loss in 2020 or if they have an increase in family size, they may be able to claim an additional credit of the difference when the individual files their 2020 tax federal income tax return in 2021.

- The IRS has confirmed that Veterans Affairs benefits recipients will automatically receive the $1200 Economic Impact Payment. No additional action by these individuals is needed, except to claim dependants under the age of 17.

- The Treasury and IRS launched the new "Get My Payment" app, which offers features for taxpayers to check on the status of their Economic Impact Payment, as authorized under the bipartisan CARES Act, as well as to update direct deposit information if needed. This app is free to use, and it's a useful tool for people who need to secure these resources quickly. "Get My Payment" is updated once daily, usually overnight, and taxpayers are urged to only use "Get My Payment" once a day given the large number of people receiving Economic Impact Payments. To access the app, visit IRS.gov and click on "Get My Payment" to fill out your information.

- The U.S. Treasury and IRS have launched a new tool to help non-filers register for Economic Impact Payments – the direct payments authorized by the bipartisan CARES Act. The non-filer tool is free to use, and it's an option designed for people who don't have a return filing obligation, including those with too little income to file. To access the feature, visit IRS.gov and click on "Non-filers: Enter Payment Info Here" where you'll then be prompted to provide basic information including Social Security number, name, address, and dependents which will be used to confirm eligibility and calculate and send an Economic Impact Payment.

Resources

- IRS: Corinavirus tax information

- IRS: Economic impact payments: What you need to know

- Committee on Ways & Means fact sheet & FAQ on direct payments

- Committee on Ways & Means FAQ on Social Security and direct payments

Resources for Small Businesses

Bipartisan Congressional and federal action has opened up new resources for small businesses hard-hit by the spread of COVID-19.

- Click here for the "Small Business Owners Guide to the CARES Act," which provides information about the major programs available through the Small Business Administration (SBA) to address financial needs and tax provisions that are outside the scope of SBA.

- Click here for a flow chart from the House Small Business Committee which provides basic information for new programs and counseling resources.

Key Small Business Programs and Resources:

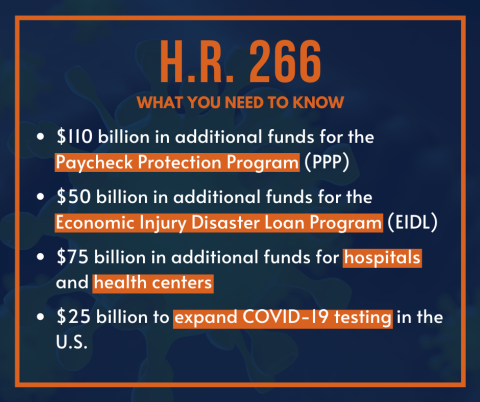

Paycheck Protection Program (PPP) – Congress created this $350 billion program to provide cash-flow assistance through 100 percent federally-guaranteed loans to employers who maintain payroll obligations during this emergency. If employers maintain their payroll, the loans will be forgiven. On April 23rd, Congress passed H.R. 266, an interim supplemental funding package authorizing an new round of $310 billion in funding for PPP after the initial $350 billion of funding for the program was expended.

Important information about the program:

- PPP provides small business with loans of up to $10 million to cover payroll and certain other expenses – loans are determined by 8 weeks of prior average payroll plus an additional 25% of that amount.

- Loan Forgiveness: If you maintain your workforce, the program includes loan forgiveness: SBA will forgive the portion of the loan proceeds that are used to cover the first 8 weeks of payroll and certain other expenses following the origination of the loan SBA will forgive all PPP loans if all employees are kept on the payroll for 8 weeks and the money is used for payroll, rent, mortgage interest, or utilities

- Payroll costs include salary wages, commissions, and tips capped at $100,000 for each employee. It also includes benefits for vacation, family and medical leave, sick leave, and other limited benefit categories.

- Eligible businesses include: qualified small businesses, 501(c)(3) nonprofits, tribal business, and veterans organizations organized under 501(c)(9) that meet the SBA's standard business size definition. Self-employed individuals, independent contractors, and sole-proprietors also are eligible.

- Restrictions: Businesses that have pending or existing SBA disaster assistance loans can still receive funding through PPP as long as new loans are not being used for the same purpose. Businesses that have an insurance claim pending may also apply for loans through this program. A single business cannot apply for more than one PPP loan.

- Application: You can apply through any existing SBA 7(a) lender or through any federally-insured depository institution, federally insured credit union, or Farm Credit System that is participating. Other regulated lenders will be available to make these loans once they are approved and enrolled in the program. You should consult with your local lender as to whether it is participating in the program. Click here to locate a qualified lender in your area.

- Key Dates: Starting April 3, 2020, small businesses and sole proprietorships can apply for and receive loans to cover their payroll and other certain expenses through existing SBA lenders. Starting April 10, 2020, independent contractors and self-employed individuals can apply for and receive loans to cover their payroll and other certain expenses through existing SBA lenders.

- Need to check on status of your application? For PPP, please contact the lender that you applied with, as they will have your information and application status. For EIDL, please contact the SBA Office of Disaster Assistance at 1-800-659-2955

Application Dates:

- Starting Friday, April 3rd, small businesses and sole proprietorships seeking to enroll in PPP can apply through existing Small Business Administration (SBA) lenders.

- Starting Friday, April 10th, independent contractors and self-employed individuals can apply for and receive loans to cover their payroll and other certain expenses through existing SBA lenders.

- To find an eligible SBA lender, visit: Sba.gov/paycheckprotection/find

For more information:

- SBA: Paycheck Protection Program Information Page

- Treasury: Assistance for Small Businesses: updated information on the program, including information for lenders. Through this resource you can find:

- List of Current SBA Lenders in Connecticut

Economic Injury Disaster Loans (EIDL) – Lower interest loans of up to $2 million, with principal and interest deferment available for up to four years, that are available to cover expenses that would have been met had the disaster not occurred, including payroll and other operating expenses. On April 23rd, Congress passed H.R. 266, an interim supplemental funding package authorizing an new round of $50 billion in funding for EIDL after the initial funding for the program was expended.

Emergency Economic Injury Grants – Provide an emergency advance of up to $10,000 to small businesses and private non-profits harmed by COVID-19 within three days of applying for an EIDL. To access the advance, you must first apply for an EIDL and then request the advance. The advance does not need to be repaid under any circumstance and may be used to keep employees on payroll, to pay for sick leave, meet increased production costs due to supply chain disruptions, or pay business obligations, including debts, rent, and mortgage payments.

Small Business Debt Relief Program – This program will provide relief to small businesses with non-disaster SBA loans, in particular 7(a), 504, and microloans. Under it, SBA will cover all loan payments on these SBA loans, including principal, interest, and fees, for six months. This relief will also be available to new borrowers who take out loans within six months.

Resources

- SBA Covid-19 resource page

- Connecticut SBA Office – resource for assistance with applying, eligibility questions, and other needs

- The Connecticut Small Business Development Centers have a dedicated resource center for small businesses struggling with the effects of COVID-19 on their workforce and ability to remain open. The CT SBDC will continually update the resource center as more information from the CARES Act becomes available.

Paid Leave for Working Americans

Under the Families First Coronavirus Response Act, employers with under 500 employees are required to provide their workers with paid sick leave and paid family leave to care for a child home due to school closures.

- For paid sick leave, employees are eligible to take up to 80 hours (two weeks) of paid time, depending on the employee's regular schedule, at 100% of the employee's regular rate of pay (up to $511 per day) due to quarantine/isolation order, health-care provider guidance to self-quarantine, or seeking diagnosis for symptoms of COVID-19; the pay is limited to two-thirds of the employee's regular rate of pay (up to $200 per day) for caring for someone who is isolated/quarantined and for taking care of a child due to a closure of school or child care.

- For paid family leave, employees are eligible to take up to 10 additional weeks of paid time at two-thirds of the employee's regular rate of pay (up to $200 per day) solely to take care of a minor child due to a closure of school or child care or the unavailability of a child care provider.

Resources

- Committee on Education and Labor Fact Sheet: Who is Eligible for Leave link

- U.S. Department of Labor Fact Sheet for Employees

- U.S. Department of Labor Fact Sheet for Employers

- U.S. Department of Labor Questions and Answers

- U.S. Department of Labor questions & answers document about employer posting requirements, as well as a Field Assistance Bulletin describing the 30-day nonenforcement policy.

- Treasury, IRS & Department of Labor Announcement link.

Resources for Student Loan Borrowers

If you have student loan debt, borrowers have several options to help provide relief through September 30, 2020. During this period, a borrower is able to:

- Pause payments for federal student loan borrowers who have Direct Loans or Federal Family Education Loans (FFEL), meaning the borrower is not required to make any payments toward outstanding interest or principal balance.

- Suspend interest accrual for loans so balances do not accrue.

- Avoid forced collections such as garnishment of wages, tax refunds, and Social Security benefits.

- Halt negative credit reporting.

- Ensure a borrower continues to receive credit toward Public Service Loan Forgiveness, Income-Driven Repayment forgiveness, and loan rehabilitation.

Additional Updates:

According to a recent update by the US Department of Education: "To provide relief to student loan borrowers during the COVID-19 national emergency, federal student loan borrowers are automatically being placed in an administrative forbearance, which allows you to temporarily stop making your monthly loan payment. This suspension of payments will last until Sept. 30, 2020, but you can still make payments if you choose." Click here to review other recent updates and announcement about student loans.

Governor Ned Lamont and Banking Commissioner Jorge Perez, in collaboration with other states, have announced that the State of Connecticut has secured relief options with many private student loan servicers whose borrowers are not covered by the recently adopted federal CARES Act. This new initiative will benefit Connecticut residents with privately held student loans.Under this new initiative, Connecticut residents with commercially owned Federal Family Education Loan Programs or privately held student loans who are struggling to make their payments due to the COVID-19 pandemic will be eligible for expanded relief. Borrowers in need of assistance should immediately contact their student loan servicer to identify the options that are appropriate to their circumstances. Relief options through the servicers listed below include:

- Providing a minimum of 90 days of forbearance;

- Waiving late payment fees;

- Ensuring that no borrower is subject to negative credit reporting;

- Ceasing debt collection lawsuits for 90 days; and

- Working with borrower to enroll them in other borrower assistance programs, such as income based repayment.

To determine the types of federal loans residents have and who their servicers are, borrowers can visit the U.S. Department of Education's National Student Loan Data System (NSLDS) or call the Federal Student Aid Information Center at 1-800-433-3243 or 1-800-730-8913 (TDD). Borrowers with private student loans can check the contact information on their monthly billing statements.

An up-to-date list of participating private student loan servicers will be maintained on the Connecticut Department of Banking's website at www.ct.gov/dob.

Resources

- For additional guidance on how to apply and learn about next steps as this critical relief becomes available, please refer to the U.S. Department of Education's Student Aid Administration website.

- If you need assistance contacting your student loan servicer or have additional questions after referring to the Student Aid Administration's guidance, please contact my Norwich office at 860-886-0139

Food Assistance and Food Banks

Congress has taken action to reinvest in the Supplemental Nutrition Assistance Program (SNAP), the Special Supplemental Nutrition Program for Women Infants and Children (WIC), and has secured $850 million in emergency funding for The Emergency Food Assistance Program (TEFAP) to help food banks facing increased demand. Click here for more information on how to access food and nutrition assistance in eastern Connecticut.

Where can Connecticut students receive their school meals during the COVID-19 pandemic?

USDA and the CT Department of Education has approved two COVID-19 Emergency Meal Programs. Lists of food pick-up locations will be continuously updated, check back for more updates and information:

- COVID-19 Emergency Meal Program Limited to Students Attending School in Specific Districts: School districts on this list are only authorized to serve meals to students enrolled in their schools, and other children age 18 or younger residing in the same household. Click here to view this list. Families should check with their local schools for instructions on meal distributions.

- COVID-19 Community-wide Emergency Meal Program for Children: ANY child 18 years or younger can receive meals at any meal service and distribution sites in these towns/cities. They DO NOT have to be a resident or attend school in these towns/cities. Click here to view this list.

Resources

- For information on applying for SNAP in Connecticut, click here.

- To learn about applying for WIC in Connecticut, click here.

- Committee on House Agriculture Fact Sheet and FAQs on anti-hunger programs

- U.S. Department of Agriculture's Coronavirus Nutrition Response

- To find food assistance near you, call the USDA National Hunger Hotline 1-866-3-HUNGRY/1-877-8-HAMBRE

- Click here to find a local food bank near you

Important Information for Veterans

Congress provided robust emergency funding to ensure the Department of Veterans Affairs (VA) has the equipment, tests, and support services – including setting up temporary care sites, mobile treatment centers, and increasing telehealth visits to allow more veterans to get care at home – necessary to provide veterans with the additional care they need. For further guidance as this funding and initiatives are implemented, please refer to the U.S. Department of Veterans Affairs website.

Important Information for you to know:

- VA health facilities in Connecticut have restricted access and altered operations in response to COVID-19. Please click here for the latest information and updates Connecticut VA operations.

- Veterans are eligible to receive the federal direct payments.

- If you are a veteran-owned small business, you can receive support through the Small Business Paycheck Protection Program to cover 8-weeks of your payroll, the mortgage interest, rent, and utility costs. There will be up to 100% loan forgiveness options for a veteran-owned small businesses that protects/fully maintains their workers.

- Under the CARES Act, federally backed mortgages, including those guaranteed or insured by the VA are protected from foreclosure for 60 days beginning on March 18, 2020. If borrowers are facing financial hardship, they can by requesting a forbearance for up to 6 months, with a possible extension for another 6 months, through their mortgage holder.

- For veteran students who are attending college through their veteran education benefits, Congress passed a measure to ensure theVA continues to make housing allowance payments to students using VA education benefits at the on-campus rate, even if the school converted to online education due to COVID-19.

- The IRS has confirmed that Veterans Affairs benefits recipients will automatically receive the $1200 Economic Impact Payment. No additional action by these individuals is needed, except to claim dependents under the age of 17.

Resources

- For further guidance as this funding and initiatives are implemented, please refer to the VA website.

- Additional Resource: VA FAQ on COVID-19

- Additional Resource: List of all VA Medical Centers

- Additional Resource: Veterans Crisis Line 1-800-273-8255

Homeowner and Renter Insurance

Congress has enacted protections for certain homeowners and renters:

- Mortgage Forbearance: Homeowners with FHA, USDA, VA, or Section 184 or 184A mortgages (for members of federally-recognized tribes) and those with mortgages backed by Fannie Mae or Freddie Mac have the right to request forbearance on their payments for up to 6 months, with a possible extension for another 6 months without fees, penalties, or extra interest. Homeowners should contact their mortgage servicing company directly or contact a HUD approved housing counselor. Contact information for a homeowner's mortgage servicer can be found in monthly mortgage statements or coupon book. The nearest housing counselor can be found at www.consumerfinance.gov/find-a-housing-counselor.

- Eviction Protections: Renters residing in public or assisted housing, or in a home or apartment whose owner has a federally-backed mortgage, and who are unable to pay their rent, are protected from eviction for 4 months. Property owners are also prohibited from issuing a 30-day notice to a tenant to vacate a property until after the 4-month moratorium ends. This protection covers properties that receive federal subsidies such as public housing, Section 8 assistance, USDA rural housing programs, and federally-issued or guaranteed mortgages. Renters whose landlord is not abiding by the moratorium should contact the relevant federal agency that administers their housing program or their local Legal Aid office.

In addition, the state of Connecticut has partnered with over 50 credit unions and banks in Connecticut to offer mortgage relief to the state's residents and businesses who continue to face hardship caused by the global COVID-19 pandemic. Under the agreement, participating financial institutions are now offering mortgage-payment forbearances of up to 90 days, which will allow homeowners to reduce or delay monthly mortgage payments. Click here for more information about this program and a list of participating financial institutions.

Additional Updates

On 4/27/2020 the Federal Housing Finance Authority (FHFA) announced updated guidance regarding the repayment terms for mortgage holders with federal backed mortgages (Fannie Mae, Freddie Mac, USDA, VA, Section 184 or 184A) who have requested forbearances due to the pandemic. There had been a concern that repayment would result in a balloon payment following the requested forbearance period. FHFA has directed servicers of these mortgages to explore the following repayment options:

- Set up a repayment plan which could spread the amount owned over an agreed term;

- Modify the loan so that the borrowers payments are added to the end of the mortgage; or

- Set up a modification that reduces the borrower's monthly mortgage payment.

For complete information on FHFA's announcement visit the media advisory here. To find out if you have a Fannie Mae or Freddie Mac backed-loan visit their Loan Look-Up tools at the links below or ask your mortgage servicer –

On April 10th Governor Ned Lamont issued a state-wide executive order (No. 7x) which enacted a series of protections for residential renters – including a 60-day grace period in rental payments for those financially impacted by the pandemic. Please visit the State of Connecticut's Homeowners and Renters page for complete information.

Support for Eastern Connecticut Farmers

Farmers in eastern Connecticut and across the U.S. are absolutely essential to our nation's food supply, and they're facing a collapse in commodity prices amid the COVID-19 pandemic. Rep. Courtney is the co-chairman of the bipartisan Congressional Dairy Caucus, and has voted on a bipartisan basis to authorize new resources for farmers and agricultural enterprises, who often operate like small businesses themselves.

- The bipartisan CARES Act established the SBA's Paycheck Protection Program (PPP) to provide $350 billion in 100% federally guaranteed loans to employers who maintain payroll obligations during this emergency. H.R. 266 replenished the program with another $310 billion. That assistance was always meant to be accessible to farmers, but SBA did not provide clear guidance when the program initially launched.

- Rep. Courtney has since secured new guidance from SBA that farmers are indeed eligible for funding through the Paycheck Protection Program. For more information on the new guidance, click here.

- The CARES Act also established the Economic Injury Disaster Loan (EIDL) and grant program, a popular program that was quickly exhausted following the bill's passage on March 27th. Farmers weren't deemed eligible for the first round of funding, so Courtney urged SBA Administrator Carranza to make sure they were eligible before Congress voted to replenish the program with H.R. 266.

- H.R. 266 passed the House on April 28 and was signed into law, and it included language that explicitly expanded EIDL eligibility to farmers.

-

The Small Business Administration (SBA) announced that, following correspondence from my colleagues and I on the Congressional Dairy Caucus, they will begin accepting new Economic Injury Disaster Loan (EIDL) and grant applications on a limited basis specifically to provide relief to American farmers and agriculture businesses. For the SBA's full announcement, and for more information on how to apply for the EIDL program, click here.

Resources

- SBA: Paycheck Protection Program Information Page

- SBA: Economic Injury Disaster Loan Information Page

- Congressman Courtney's Op-Ed in the JI

Legislative Action & Press Releases

Congress has passed three pieces of legislation designed to respond to the public health needs of states and localities, as well as the financial needs of families, community organizations, and small businesses.

On March 6th, Congress passed the Coronavirus Preparedness and Response Supplemental Appropriations Act to provide $8.3 billion in emergency funding to state and local public health departments.

On March 18, the Families First Coronavirus Response Act was signed into law to provide emergency paid leave to working Americans affected by Coronavirus, provide free COVID-19 testing, bolster state funding for Unemployment Insurance, and increase access to school and senior nutrition programs during the crisis.

Most recently, the Coronavirus Aid, Relief, and Economic Security (CARES) Act was passed to provide direct financial relief to struggling families, individuals who are out of work, and businesses affected by the Coronavirus.

On April 23rd, the House passed a fourth bipartisan bill, H.R. 266 meant to provide stop-gap funding to critical programs, allocate more money for hospitals, and fund a robust COVID-19 testing program.

Press Releases

- Rep. Courtney Statement On Passage Of Supplemental Funding Package To Curb Spread Of Coronavirus Rep. Courtney Shares New Update On House's Work To Address COVID-19 Outbreak Rep. Courtney Helps Introduce Two Bills To Protect Americans Amid COVID-19 Outbreak Rep. Courtney Votes For Coronavirus Economic Relief Package Courtney Releases Statement, Pens Op-Ed On Administration's Failure To Protect Student Borrowers Amid COVID-19 Outbreak Courtney Statement On Senate Approval Of House-Passed COVID-19 Response Package Rep. Courtney Introduces Bill To Cover Full Cost Of Future COVID-19 Vaccine Rep. Courtney Statement On Senate GOP Coronavirus Bill Courtney Joins Over 100 Bipartisan Colleagues Demanding Support For First Responders Courtney Statement On Senate Coronavirus Bill Agreement\ Rep. Courtney Bill To Cover Full Cost Of COVID-19 Vaccine Included In Senate's Bipartisan Coronavirus Agreement Courtney Introduces Bill To Give Student Borrowers A Fair Deal In The Road To Economic Recovery Amid COVID-19 Pandemic Courtney Announces New Federal Grant Awards To Support COVID-19 Response Efforts In Willimantic And Norwich Courtney Statement On House Passage Of The Bipartisan CARES Act Rep. Courtney Statement On FEMA Approval Of Connecticut's Request For Major Disaster Declaration Courtney Highlights New Guidance For Small Business Owners Amid COVID-19 Outbreak">Rep. Courtney Statement On Passage Of Supplemental Funding Package To Curb Spread Of Coronavirus.

- Rep. Courtney Shares New Update On House's Work To Address COVID-19 Outbreak

- Rep. Courtney Helps Introduce Two Bills To Protect Americans Amid COVID-19 Outbreak

- Rep. Courtney Votes For Coronavirus Economic Relief Package

- Courtney Releases Statement, Pens Op-Ed On Administration's Failure To Protect Student Borrowers Amid COVID-19 Outbreak

- Courtney Statement On Senate Approval Of House-passed COVID-19 Response Package

- Rep. Courtney Introduces Bill To Cover Full Cost Of Future COVID-19 Vaccine

- Rep. Courtney Statement On Senate GOP Coronavirus Bill

- Courtney Joins Over 100 Bipartisan Colleagues Demanding Support For First Responders

- Courtney Statement On Senate Coronavirus Bill Agreement

- Rep. Courtney Bill To Cover Full Cost Of COVID-19 Vaccine Included In Senate's Bipartisan Coronavirus Agreement

- Courtney Introduces Bill To Give Student Borrowers A Fair Deal In The Road To Economic Recovery Amid COVID-19 Pandemic

- Courtney Announces New Federal Grant Awards To Support COVID-19 Response Efforts In Willimantic And Norwich

- Courtney Statement On House Passage Of The Bipartisan CARES Act

- Rep. Courtney Statement On FEMA Approval Of Connecticut's Request For Major Disaster Declaration

- Courtney Highlights New Guidance For Small Business Owners Amid COVID-19 Outbreak

Please note that as additional information becomes available, this page will be updated.